Navigating the Storm: How the U.S. Economy is Reshaping Corporate Travel in 2026

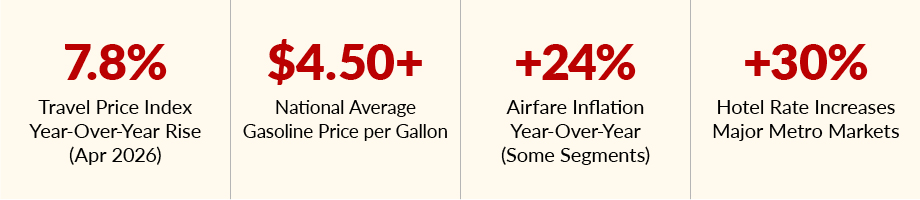

The headline numbers from the U.S. Travel Association’s April 2026 Travel Price Index are striking. Travel prices rose 7.8% year-over-year — more than twice the overall Consumer Price Index increase of 3.8%. That’s the largest annual jump since the post-pandemic rebound of 2022. The driver? An energy shock tied to ongoing Middle East conflict pushed gasoline above $4.50 per gallon nationally and oil past $100 per barrel, radiating price pressure through every mode of corporate transportation.

Fuel: The Invisible Budget Line That Just Became Visible

“The landscape will continue to be shaped by inflation, supply constraints and evolving traveler expectations. Buyers can plan with more confidence — but success will come from staying informed and flexible.”

— Suzanne Neufang, CEO, GBTA

Fuel costs are no longer a background variable in managed travel programs — they are a frontline budget issue. Airline fares surged 20.7% on an annual basis through April 2026, according to U.S. Travel Association data, reversing a brief period of softening. Hotel prices, which had declined early in the year, reversed course with a 4.3% annual increase in April as energy and labor costs hit property operations simultaneously.

Fuel surcharges are also resurfacing in ground transportation contracts. As BCD Travel’s 2026 Outlook noted, declining contract value, fuel surcharges and program leakage are the three key concerns requiring stronger sourcing strategies. Low-cost carrier options are also narrowing: In May 2026, Spirit Airlines abruptly shut down after rising fuel costs made operations untenable, further tightening capacity in leisure-heavy markets that many corporate programs rely upon for budget routes.

For travel buyers with car rental or fleet components in their programs, the pressure is compounded. Rental car pricing continues to rise due to repair costs, acquisition challenges, surcharges and parking fees. Hidden fuel surcharges embedded in ground transportation contracts are catching budget managers off guard, with industry advisors noting that all-inclusive corporate rate structures — while priced higher — frequently deliver better total cost predictability than seemingly cheaper per-trip models.

Inflation’s Broader Grip on Program Economics

Beyond fuel, the broader inflationary environment is creating compounding pressure on every line of a managed travel budget. The CPI for all items hit 3.8% annually through April — the highest rate since May 2023 — while travel-specific inflation outpaced it by a factor of two. Hotel average daily rates (ADR) in major U.S. metro markets are running 22%-30% above pre-surge baselines, driven by strong domestic travel demand, limited new hotel supply and labor cost escalation that hotel operators are passing through to buyers.

Global hotel rates are projected to increase 4.9% in 2026 overall, according to BCD Travel’s market intelligence, with variation driven by staffing costs, leisure demand competition and local tax changes. For managed programs relying on static annual rate contracts negotiated in a calmer market, the mismatch between contracted and market rates is creating significant leakage — travelers booking outside policy when preferred-property rates no longer represent competitive value.

The GBTA and CWT’s joint 2026 Annual Global Business Travel Forecast, developed through econometric modeling by the Avrio Institute, projected modest stabilization heading into the year. But that forecast carried an explicit caveat: a “downside scenario” assuming economic deterioration from trade tensions. Events have increasingly favored that scenario. Oxford Economics now projects global GDP growth at just 2.6% — the weakest pace since 2009, excluding 2020 — with inflation easing only gradually from 3.4% in 2025 to just above 3% this year.

Tariffs, Geopolitics and the Cross-Border Challenge

For companies with international travel components, the economic headwinds are compounded by policy-driven uncertainty. GBTA sounded a significant alarm earlier in 2026, warning that tariffs and U.S. entry restrictions could slash corporate travel volumes by as much as 21% if conditions deteriorate further. In a global survey of 905 travel managers, suppliers and travel professionals, 29% of travel buyers expected business travel at their companies to shrink in the near term — a sharp reversal from the growth expectations that characterized 2024 planning cycles.

GBTA CEO Suzanne Neufang was direct: “Productive and essential business travel is threatened in times of economic uncertainty or in an environment of additional barriers and restrictions. This undermines economic prosperity and damages the many sectors that rely on global business travel to survive and thrive.” Already, 7% of buyer organizations have revised travel policies specifically to or from the U.S., and the number is expected to grow as corporate risk officers reassess cross-border mobility plans.

For travel managers, this translates into real program complexity: supplier contracts built on volume assumptions that may not materialize, duty-of-care obligations in markets with shifting entry requirements and traveler anxiety that can itself drive out-of-policy booking behavior.

What Smart Buyers Are Doing Right Now

Despite the headwinds, the data does offer grounds for strategic optimism — particularly for programs willing to move from reactive cost management to proactive program design. The GBTA forecast still anticipates 8.1% global business travel spend growth in 2026, reflecting the enduring necessity of face-to-face engagement across sectors. U.S. business travel spend is forecast at $319 billion, up modestly from $317 billion in 2025.

FCM Travel’s State of the Market survey found that most travel buyers are prioritizing technology investment as their primary lever: real-time itinerary adjustments, policy compliance enforcement, fare reshopping engines, predictive analytics and automated expense tracking are the top priorities for 2026. Among companies evaluating TMC changes, 39% cite technology capability — not service volume or price — as the primary driver of their decisions.

The shift from static annual contracts to dynamic pricing strategies is accelerating across both air and hotel categories. Hotel RFPs in leading programs are moving to market-based pricing and direct negotiation, replacing the fixed-rate annual cycle that no longer reflects actual market conditions. Companies able to benchmark performance in real time and adjust preferred-supplier strategies mid-year are realizing savings of 10%-25%, according to AccessPerks industry analysis — without changing a single vendor relationship.

Behavioral economics is also proving powerful. Aligning traveler behavior through tighter but well-communicated policy can reduce per-trip costs by 14% without any change to vendor contracts. The key is frictionless compliance: programs with high online booking tool adoption consistently outperform those dependent on agent-assisted channels, which carry meaningfully higher transaction costs.

ACTION CHECKLIST FOR TRAVEL BUYERS: MID-2026 PRIORITIES

- Audit fuel surcharge exposure across all ground transportation and air contracts immediately — hidden surcharges are eroding negotiated savings

- Stress-test hotel preferred-property rates against current ADR benchmarks; leakage risk is highest in major U.S. metros where rates are up 22%-30%

- Evaluate a dynamic pricing strategy for hotel sourcing to replace static annual RFP rates in high-volatility markets

- Review cross-border travel policies in light of shifting U.S. entry requirements and traveler security assessments (ISO 31030 alignment recommended)

- Invest in fare reshopping and predictive analytics technology — these are now baseline expectations, not competitive differentiators

- Align with finance leadership using total travel spend per revenue dollar, not just gross travel expenditure, to demonstrate program ROI

- Monitor carrier capacity developments closely; Spirit Airlines’ collapse signals further low-cost carrier vulnerability as fuel prices remain elevated

The Bottom Line for Program Managers

The U.S. economy in 2026 is presenting corporate travel managers with a rare and demanding convergence: an energy shock driving transportation costs sharply higher, broad inflationary pressure on hotels and dining, geopolitical uncertainty complicating international program design and a softening economic outlook making CFOs scrutinize every discretionary line. Business travel spend is not collapsing — but the era of low-friction growth is over.

The buyers who will outperform over the next 18 months are those who treat their managed programs as strategic assets requiring continuous optimization, not administrative functions requiring periodic RFP cycles. Data, flexibility, behavioral alignment and technology investment are not optional upgrades — they are the new baseline for competitive program management in an inflationary economy.

As GBTA’s Neufang put it: “With better data and clearer trends, buyers can plan with more confidence. Success will come from staying informed and flexible, while aligning travel decisions with broader business goals.” In 2026, that is both the challenge and the mandate.

SOURCES REFERENCED IN THIS ANALYSIS

-

GBTA / CWT 2026 Annual Global Business Travel Forecast — gbta.org

-

GBTA Business Travel Index (BTI) Outlook — Annual Global Report & Forecast, July 2025

-

GBTA Global Poll: Tariffs and Entry Restrictions Impact on Corporate Travel, April 2025

-

U.S. Travel Association Travel Price Index, April 2026 — ustravel.org

-

U.S. Travel Association Spring 2026 U.S. Travel Forecast — ustravel.org

-

BCD Travel: Travel Market Report 2026 Outlook — bcdtravel.com

-

BCD Travel / Advito: What Travel Leaders Should Take Away from the 2026 Outlook

-

FCM Travel: Business Travel Trends & Strategies H1-2026 — fcmtravel.com

-

Corporate Travel Management (CTM): 2026 Corporate Travel Outlook — travelctm.com

-

AccessPerks: Corporate Travel Discounts in 2026 — blog.accessperks.com

-

Engine: 2026 Business Travel Season Forecast — engine.com

-

NerdWallet Travel Inflation Report, May 2026 — nerdwallet.com

-

Business Travel News Europe: The 2026 Outlook — businesstravelnewseurope.com

-

Business Traveler USA: GBTA Sounds the Alarm — businesstravelerusa.com

Learn more about this featured business travel agency near you

For more details, connect with this friendly, knowledgeable travel agency today.